A long update on shipping as Our Man took advantage of the pullback in product and crude tankers, and the increasing proximity of IMO 2020, to increase his Shipping position to 15% at the end of Q3.

Unless IMO 2020 proves to be a completely damp squib (think Y2K!), it’s a position that Our Man doesn’t expect to trade much for the next year or so. However, should tanker companies start to trade at multiples of NAV or you hear people mention them as “high dividend” stocks let Our Man know, as it will definitely be time to get out of dodge!

An update to the broad rationale for the thesis is below, though OM will spend less time talking about IMO 2020 and its impacts (see this piece for more on that).

Also, while the thesis holds broadly true for shipping generally, OM’s investment is in Crude Tankers and Clean Product Tankers** and so the below is focused on those.

------------------------------------------------------------------------------------------------

MASSIVE CAVEAT EMPTOR

Shipping is a terrible industry to invest in!

It is a cyclical business with high fixed costs and low operating costs that leads to ugly economics. Where else could you lever up to buy an asset that has a 20-year life but which is only profitable for 6-8 quarters of that life cycle! Historically, this has been compounded by largely untrustworthy management teams who have engaged in all kinds of self-dealing transactions! Meanwhile, in shipping’s rare moments of profitability, lenders have been foolish enough to loan ship-owners more money and ship-owners have ordered yet more vessels. This has led to an excess supply of vessels that destroys the industry’s future profitability!

So, what is OM doing and why now??

Well, the thesis is a fairly prototypical example of the type of dislocation OM likes; beaten-down stock prices, investor disinterest, attractive valuations and fundamental trends, and something that will change the narrative.

Shipping is a terrible business that’s been oversupplied for years leading to collapsing share prices, investors ignoring it and attractive valuations. This excess supply and subsequent losses led to bankruptcies/restructurings which saw lenders taking losses and equity issuance from the surviving companies and no capital to finance new vessels. Meanwhile, a major regulatory change (IMO 2020) is being enacted on January 1st, 2020 and will potentially cause further disruption to both supply and demand.

Our Man has discussed the attractiveness of optionality in investments before. In Shipping, the operational and financial leverage means that for all of the sector’s many warts, in those 6-8 quarters that a vessel is profitable you make so much $$$ that it pays for the entire vessel! Our Man believes we are at one of those inflection points due to the combination of the companies already being around break-even, the constrained supply of new vessels, attractive pricing and trends, and the potentially disruptive impact of IMO 2020.

Background since the financial crisis

Since Great Recession, shipping has been a story of oversupply and bad rates! Whenever there were brief respites and shipping rates increased, investors lent money, ship owners ordered more ships, and rates got crushed as this new supply entered the market. Unsurprisingly, this led to falling stock prices, defaults and massive dilution for equity holders. It has also meant that many of the lenders to shipping companies (especially German banks/retail investors!!!) have exited the market.

OM’s largest position is Scorpio Tankers (STNG); this is what its stock price has done since its IPO in early 2010...

|

| Source: Koyfin |

Yup, that’s a fall from the $130 (split adjusted) IPO price to a low of $15 in late 2018!

Valuation

Unsurprisingly, after restructurings that saw debt holders suffer meaningful haircuts and further equity raises, investors have not been too keen on the shipping sector! Valuation reached an extreme in late 2018 and early 2019, when crude and product shipping companies traded for about 50-70% of their book value despite seeing stronger rates and with IMO 2020 on the horizon. Though the stocks have risen meaningfully since the start of the year, they still trade at a discount to book value. This is with rates still stronger than prior years and IMO 2020 only now starting to penetrate generalist investors’ consciousness.

Supply, Demand and Rates

As the chart below suggests, the order book for Crude tankers is near the lows of the last ~25 years and this dynamic is further improved by the increasing age of the fleet*. The story is the same for Product tankers, where the order book is the lowest (as % of the fleet) since March 2000. This discipline has largely been driven by shell-shocked management teams following the (often multiple) restructurings coupled with the limited new capital available to the sector.

|

| Source: Clarksons, from Euronav October Presentation (Pg. 18) |

On the demand-side, oil demand has grown incrementally by a couple of percent per annum over the last 2 decades and is projected to continue its slow growth for the next few years (the IEA predicts a plateau in 2030!). More importantly there is a major structural change in the marginal exporter of crude and petroleum products, with the US taking over this role from the Middle East. The discovery of shale oil has led to the US being responsible for up to 85% of the global increase in oil production. This has seen US exports of crude oil double since the start of 2018. Petroleum products show a similar story and should accelerate in 2020 as new pipeline capacity to refiners comes online.

This transition to US exports really matters to shipping companies.

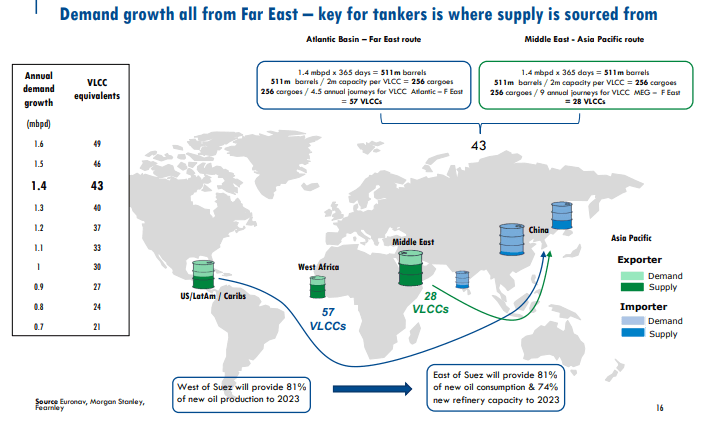

Why? Geography!

The key for crude and product companies is where supply is sourced. It takes about twice as long for tankers to travel from the US to Asia, compared to from the Middle East and it requires twice as many tankers. As a ship-owner, that’s a meaningful increase in demand! With the supply of vessels fixed in the short-term, and limited new vessels on order, even small changes in demand can have major impacts on rates. Examples of this can clearly be seen historically;

Why? Geography!

The key for crude and product companies is where supply is sourced. It takes about twice as long for tankers to travel from the US to Asia, compared to from the Middle East and it requires twice as many tankers. As a ship-owner, that’s a meaningful increase in demand! With the supply of vessels fixed in the short-term, and limited new vessels on order, even small changes in demand can have major impacts on rates. Examples of this can clearly be seen historically;

|

| Source: Clarksons Research Services Ltd, Clarksons Platou Securities Inc. From Marine Money presentation (slide 7) |

The impact of these changes on rates has a material impact on profitability given the operating leverage (high fixed costs, low operating costs) inherent in the business model. For an example, take the example of the crude tanker company Euronav. The chart below, from Euronav’s October investor presentation, shows management’s guidance on the impact on EBITA (a measure of profitability) of an increase in rates. OM will spare you the math, but the middle scenario below (with VLCC rates of $40K) would lead to earnings of ~$1.40/share on a stock that’s trading at $11 today.

|

| Source: Euronav October 2019 presentation (slide 8) |

Given the tightness of the market, and the impact on rates, could rates go much higher than $40K for VLCC's?? Take a look at that rates chart above!

Something to Change the Narrative: IMO 2020

The improvements in the supply/demand, and the valuation support, make the shipping thesis interesting but it’s the possible disruption from and investor attention caused by the IMO 2020 regulations that leads to the outsized position. What is IMO 2020?

- Well, it’s a new regulatory regime that prohibits vessels from using high-sulfur fuel oil (HSFO) unless they can capture the pollution causing materials. The allowed sulfur content is falling dramatically from 3.5% to 0.5%.

- There is no ease-in or adjustment period. Jan 1st, 2020 is the drop-dead date for compliance.

- Ship operators have a limited number of choices: Use low-sulfur marine gas oil (MGO), retrofit their ships to use liquefied natural gas, slow-steam (i.e. take longer to do a route, effectively reducing supply) or install scrubbers (to capture the pollution causing materials).

- Scrubbers are a popular choice but are expensive ($1-10mn/ship) and vessels have to be dry-docked, and removed from service, for them to be fitted. This temporarily reduces supply.

- Given the costs of the various options for IMO 2020 compliance a number of older ships are expected to be retired, reducing the supply of vessels.

For crude and product tankers, in addition to the likely supply side impacts above, OM thinks that there will also be positive demand-side impacts! There’s now a price on sulfur content in oil and this will likely cause changes in refinery demand, and oil trade routes. If you want to read more on OM’s IMO 2020 thoughts, you can right here!

Some Risks To the Thesis:

A far from extensive list includes:

- It’s shipping! Did you not read the caveat emptor – it’s a terrible, horrible, no good, very bad industry.

- A global slowdown could impact oil demand, meaning headwinds for both the companies and the stocks.

- IMO 2020’s impact could be more akin to Y2K, meaning that rates wander around current levels.

- Common perception is that an escalation in the 'trade war' between the US and China would be bad. Our Man is a little more sanguine on that as trade wars mean the disrupting of old trade routes, and the creation of new and less efficient ones.

-------------------------------------------------------------------------------------------------------

* Vessels over 15yrs old have to be surveyed more frequently (2.5yrs vs. 5yrs) and the cost of this increases with the age of the vessel (~$4mn for a 20yr old ship vs. ~$2mn for a 10yr old vessel)

** Crude Tankers transport unrefined crude oil to refineries, and Product Tankers move the refined oil products (e.g. light petroleum products) to points near consuming markets.

Disclaimer: As noted above Our Man holds positions in crude and product tanker

companies, specifically he has positions in Scorpio Tankers (STNG), Euronav (EUR) and Diamond S

Shipping (DSSI).

{kind=link}