Portfolio Update

On Monday morning, OM exited the small residual position in the Nasdaq Biotech ETF (IBB) within the Thematic – 4th Industrial Revolution names.

OM also added the portfolio’s first short, Short…the Nasdaq Biotech ETF (the 2x levered inverse ETF – BIS - as there is no single levered version), which represents 10% of capital (leverage-adjusted).

Short: Biotech

If you have ever spent time with professional investors, which describes a portion of Our Man’s day job, you’ll quickly hear some truisms about the short-side; (i) don’t short good companies (or those with secular tailwind), (ii) don’t short on valuation grounds and (iii) for heaven’s sake don’t do it when the stock has price momentum and is rising quickly. There are good reasons why professional investors hold these views; high quality businesses/management create options for themselves (and easy to understand secular stories offer a strong multi-period tailwind), an expensive stock can get more expensive (see Tesla, to many a short’s chagrin…so far!), and as the saying goes “the trend is your friend until it hits a bend”. Most who have shorted to any degree have been caught on the wrong side of one of these truisms, and sometimes on the wrong side of all three – even those who should know better.

So, why start with this public service announcement on short selling. Well, because if you have ever spent time with professional short-sellers (i.e. short-selling is MOST of what they do) you will have learned that some of the BEST shorts violate those rules, but that context matters! In essence, investors should be so certain in their position that complacency has set in. The secular theme should be regarded as obvious (or the company as close to flawless) and the valuation should be either ‘new’ or accepted as appropriate without the requisite thought to whether they make sense. Additionally, the stock should have performed exceptionally well for a prolonged period (strong momentum) - this helps create substantial unrealized profits, complacency in analysis and substantial downside (especially in combination with the valuation). Finally, and most importantly, that price trend should have already hit its bend – missing the first 10% of a move is less important than timing it right, since the downside is substantial.

So why Biotech, and why now?

- Company/Trend:

Our Man has talked about the secular trend in biotechnology – in this, his opinion has changed little BUT the context is that it is a long-term trend and expectations have overshot current reality.

- Valuation:

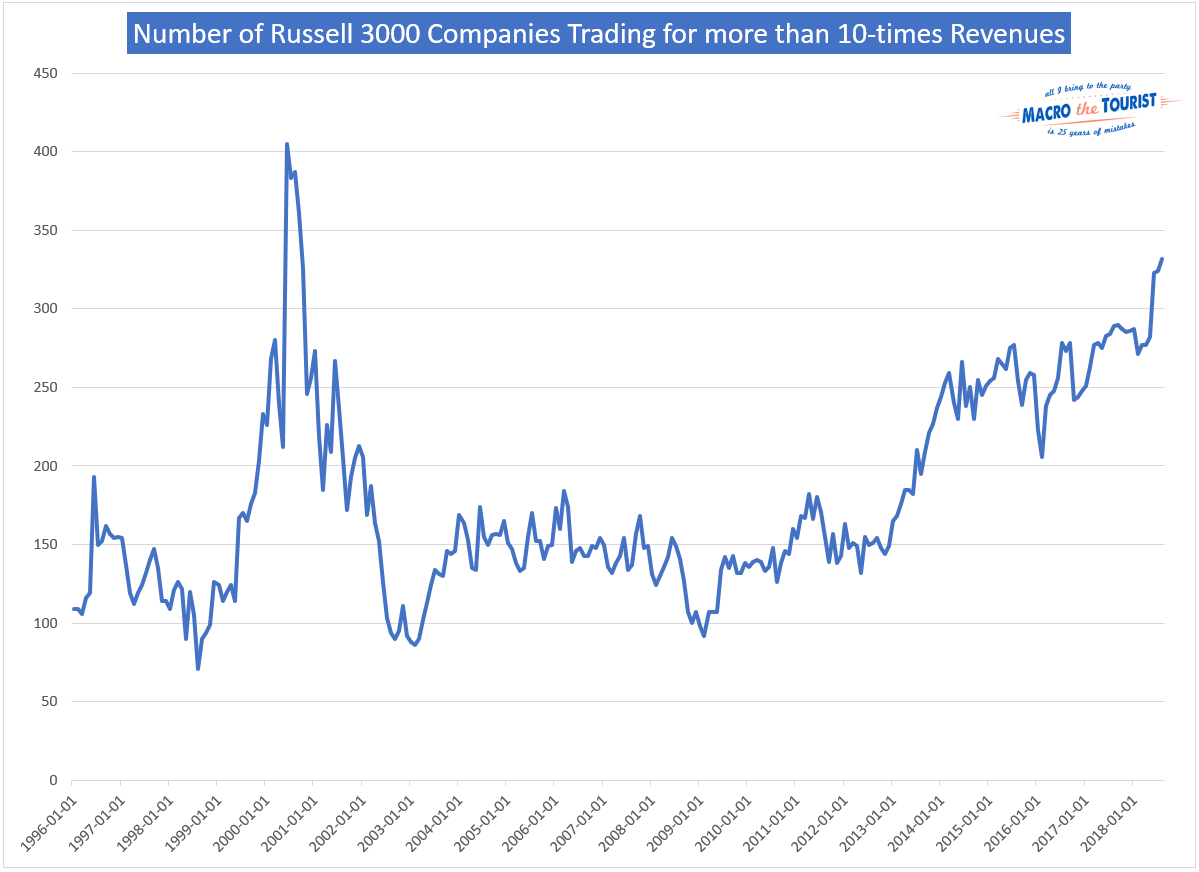

To help think about valuation in context, here’s a 2002 quote from Scott McNealy, the former CEO of Sun Microsystems (which traded at 10x revenue in 2000).

“At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?”

In short, the only ways that 10x revenue is not an absolutely crazy multiple is (i) if you’re a quasi-monopoly/oligopoly that’s growing double digits and already has huge margins (we can see you Visa and Mastercard), or (ii) you’re about to turn into one of those companies (i.e. insane revenue growth with future high margins)

For those of OM’s vintage (or older) 1999/2000 were heady days, a mass hysteria of craziness that was never to be repeated…right?

Well…the excellent Keith Muir (The Macro Tourist) posted this chart a couple of weeks ago.

On Monday morning, OM exited the small residual position in the Nasdaq Biotech ETF (IBB) within the Thematic – 4th Industrial Revolution names.

OM also added the portfolio’s first short, Short…the Nasdaq Biotech ETF (the 2x levered inverse ETF – BIS - as there is no single levered version), which represents 10% of capital (leverage-adjusted).

Short: Biotech

If you have ever spent time with professional investors, which describes a portion of Our Man’s day job, you’ll quickly hear some truisms about the short-side; (i) don’t short good companies (or those with secular tailwind), (ii) don’t short on valuation grounds and (iii) for heaven’s sake don’t do it when the stock has price momentum and is rising quickly. There are good reasons why professional investors hold these views; high quality businesses/management create options for themselves (and easy to understand secular stories offer a strong multi-period tailwind), an expensive stock can get more expensive (see Tesla, to many a short’s chagrin…so far!), and as the saying goes “the trend is your friend until it hits a bend”. Most who have shorted to any degree have been caught on the wrong side of one of these truisms, and sometimes on the wrong side of all three – even those who should know better.

So, why start with this public service announcement on short selling. Well, because if you have ever spent time with professional short-sellers (i.e. short-selling is MOST of what they do) you will have learned that some of the BEST shorts violate those rules, but that context matters! In essence, investors should be so certain in their position that complacency has set in. The secular theme should be regarded as obvious (or the company as close to flawless) and the valuation should be either ‘new’ or accepted as appropriate without the requisite thought to whether they make sense. Additionally, the stock should have performed exceptionally well for a prolonged period (strong momentum) - this helps create substantial unrealized profits, complacency in analysis and substantial downside (especially in combination with the valuation). Finally, and most importantly, that price trend should have already hit its bend – missing the first 10% of a move is less important than timing it right, since the downside is substantial.

So why Biotech, and why now?

- Company/Trend:

Our Man has talked about the secular trend in biotechnology – in this, his opinion has changed little BUT the context is that it is a long-term trend and expectations have overshot current reality.

- Valuation:

To help think about valuation in context, here’s a 2002 quote from Scott McNealy, the former CEO of Sun Microsystems (which traded at 10x revenue in 2000).

“At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?”

In short, the only ways that 10x revenue is not an absolutely crazy multiple is (i) if you’re a quasi-monopoly/oligopoly that’s growing double digits and already has huge margins (we can see you Visa and Mastercard), or (ii) you’re about to turn into one of those companies (i.e. insane revenue growth with future high margins)

For those of OM’s vintage (or older) 1999/2000 were heady days, a mass hysteria of craziness that was never to be repeated…right?

Well…the excellent Keith Muir (The Macro Tourist) posted this chart a couple of weeks ago.

When you start parsing through

the list of names, two sectors stand out Healthcare (especially Biotech) and

Technology.

So, why short just Biotech not Technology?

- Well, OM uses a very blunt instrument (an inverse ETF) to short rather than finding specific names and so general traits are more important than individual names.

- For technology companies, OM can see the argument that true subscription software companies should see higher valuations that their historical peers. For these companies, as they scale the marginal cost* approaches 0%. For example, it costs Adobe Creative Cloud/Netflix/etc. (almost) nothing to add an extra customer – no shipping costs and the cloud-based product (Photoshop, video on demand, etc.) is infinitely divisible (i.e. me editing my holiday photos or watching “House of Cards” doesn’t stop you from doing either). As such, if these business have a large user base (or are rapidly on their way to having one) they will benefit from this low marginal cost, and deserve a revenue multiple that’s higher than it has been historically. OM suspects that Technology – and especially those companies that purport to be software companies but are not – will get their comeuppance, but the breadth of the ETF means it’s hard to have confidence in putting on that position.

- For Biotech companies, OM has had discussions with a number of professional investors over the last 6-months where a central theme has been the market’s willingness to ascribe high valuations to numerous companies in the early stages of drug development (i.e. with very limited revenues). In some cases, these valuations would be aggressive even if the drugs were in market today (as opposed to years away from market). Given the number of these companies, and the companies’ inability to control the drug approval process (and timing), the valuation gap seems compelling. While the optimal & vastly more profitable strategy would be to set-up a co-investment vehicle with one of these professional investors to short a basket of these names, OM will instead have to settle for the blunt instrument that is the ETF.

- Broken Momentum

So, why short just Biotech not Technology?

- Well, OM uses a very blunt instrument (an inverse ETF) to short rather than finding specific names and so general traits are more important than individual names.

- For technology companies, OM can see the argument that true subscription software companies should see higher valuations that their historical peers. For these companies, as they scale the marginal cost* approaches 0%. For example, it costs Adobe Creative Cloud/Netflix/etc. (almost) nothing to add an extra customer – no shipping costs and the cloud-based product (Photoshop, video on demand, etc.) is infinitely divisible (i.e. me editing my holiday photos or watching “House of Cards” doesn’t stop you from doing either). As such, if these business have a large user base (or are rapidly on their way to having one) they will benefit from this low marginal cost, and deserve a revenue multiple that’s higher than it has been historically. OM suspects that Technology – and especially those companies that purport to be software companies but are not – will get their comeuppance, but the breadth of the ETF means it’s hard to have confidence in putting on that position.

- For Biotech companies, OM has had discussions with a number of professional investors over the last 6-months where a central theme has been the market’s willingness to ascribe high valuations to numerous companies in the early stages of drug development (i.e. with very limited revenues). In some cases, these valuations would be aggressive even if the drugs were in market today (as opposed to years away from market). Given the number of these companies, and the companies’ inability to control the drug approval process (and timing), the valuation gap seems compelling. While the optimal & vastly more profitable strategy would be to set-up a co-investment vehicle with one of these professional investors to short a basket of these names, OM will instead have to settle for the blunt instrument that is the ETF.

- Broken Momentum

Applying the same technical

analysis, as inspires OM’s Technical book, suggests that the ~10-year bull

market in biotech is over with the market peak in September**. While it’s very early to make projections,

the early indications are for a substantial decline.

In summary, Biotech offers an

interesting opportunity as there’s an attractive long-term secular theme that’s

well understood but has over-extended in the short-term. The stocks are well-held, and trading at

exceptionally high valuations, and until recently they had very strong

long-term momentum. This momentum

appears to have broken leaving substantial room for re-rating.

--------------------------

--------------------------

*Yes, there are other costs like programming costs, salaries, etc. but the cost of software production is largely fixed (vs variable) and so over a very large user base tends towards 0%. These articles by Chris Kluis and Basab Pradhan talk more about the concept of (almost) zero marginal cost.

For those wanting to think more about software subscription businesses in general, you should read this fantastic article by Tren Griffin (in 25IQ, his blog).

** OEW is a technical theory that takes a quantified approach to Elliot Wave Theory. For the Biotech chart attached, the bull market has 5 waves (each marking a peak, such as 3, or a trough such as 2 or 4) which ended at [1]. The theory suggests a substantial pullback is now expected…

Disclosure: OM owns BIS, and is thus short Biotech. Shocking, given the above, I know.