Given the recent and likely ongoing volatility, OM wanted to talk about how plans on managing his Shipping positions. As such, this post is primarily a way to help OM clarify his own thoughts and commit them to paper.

An advantage of being in the investment world over the last 20-years is that OM has seen many otherwise intelligent and rational folks make appalling investment decisions. Typically, these decisions come at times of stress and often around the investor’s high conviction positions! These experiences mean that OM his keenly aware that it is as important to protect your mental capital as it is your financial capital when investing.

This is particularly the case for OM’s position in Shipping. It will be very volatile; the underlying supply/demand dynamics mean shipping rates will fluctuate significantly, the operating and financial leverage of the stocks will add to this and the terrible history of the sector means the marginal investor will initially focus too heavily on short-term data points. For Our Man’s portfolio, this is magnified further due to the size of the position – it is indubitably the highest risk position in the portfolio. That is not an oversight.

So how to deal with this volatility and the uncertainty it will naturally engender?

First of all accept it is coming and be comfortable with the consequences of that. Shipping will likely dominate the moves of OM’s portfolio over the coming weeks, months and quarters. It will happen regularly and so OM will not be writing up every 20-30% move up or down in the stocks, or adjusting the portfolio for them.

Second, remember why you’re invested. For Our Man, it’s a high conviction Dislocation position that is fully sized and ‘on the clock’ now that the catalyst (IMO 2020) to engender investor interest has occurred. The goal for Dislocation positions is that they return multiples of invested capital within a relatively defined time period. To capture the compounding required to generate this performance, OM treats them more like private-equity positions. This means, the positions aren’t really resized or traded unless (i) the long-term thesis changes or (ii) the capital at risk in the position goes beyond OM’s preset tolerance.

Currently, OM’s view is that “too much” capital at risk would be 25-30% NAV in Shipping and 10% in any of individual names. However, if OM’s thesis is correct then these max capital at risk levels will slowly decline. So while Shipping is currently OM’s highest risk position, he’s comfortable with the potential mark-to-market losses and expecting to be paid for that risk.

The difficulty of dislocation positions is that even after the ‘catalyst’ they require patience and will-power. This will particularly be the case in Shipping, and Bob Farrell’s Rule Number Four (10 Market Rules to Live By) sums up what to expect.

“Exponential rapidly rising or falling markets usually go further than you think, but they do not correct by going sideways” -- Bob Farrell

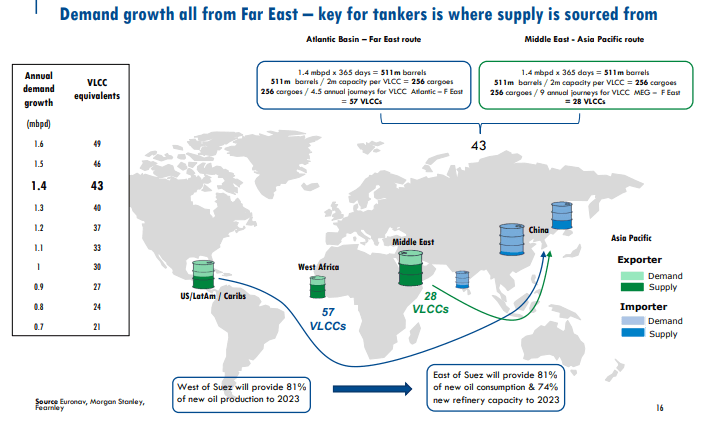

Third, have a plan! A plan is a starting point, and it should change over time as circumstances and data change. Here are the key elements to OM’s plan. OM is primarily focusing on the fundamentals - relevant crude/product tanker shipping day rates and how they show up in company earnings. He is most interested in the general level of rates and how they compare to prior years, and less so with the short term moves. The short-term changes will likely be substantial and inconsistent, and overly focusing on them is how you destroy mental capital through obsessing about the trees but missing the forest. Remember, for Dislocation investments the time horizon for the thesis is 18-24mos (max 30mos), in this case from Jan 2020, so the longer-term levels and their trends matters more. Secondly, Shipping is a very seasonal sector and so comparison to prior years is more important than vs. recent months. Obviously, strong day rates should lead to strong corporate earnings (and potentially dividends), which will help attract other investors.

Meanwhile, understand it is shipping and the crappy history that created the opportunity means that new(er) investors will be skeptical. It will take day rates being meaningfully and consistently higher than previous years, and the companies showing they’re not spending their free cash flow on more ships for the investor community to start to get very interested. Until then, every downturn in rates will lead to “it’s the end of the cycle” comments. This is another factor that will only exacerbate the volatility in both directions.

Fundamentals will also be the simplest and most important way for OM to be proven wrong. So expect him to exit if (i) the recent rise in shipping rates is brief and cyclical and then they consistently look like 2018/2019’s rates, or (ii) better rates don’t flow through to company earnings and free cash flow, or (iii) companies repeat the folly of past cycles and order new ships!

What could make OM sell if he’s right?

If OM is correct in his thesis then there are two ‘rules’ – on position size and holding period – for Dislocation positions in addition to any qualitative rationale, for reducing/exiting positions. As mentioned about these rules are of a typical holding period of 18-24 months (and 30 months maximum) from the narrative changing event (IMO 2020 on Jan 1st, 2020), and OM has set the maximum position size he’s comfortable with at 25-30% today (and 10% per individual position) though both will decline as the thesis progresses.

Assuming the fundamentals continue to trend well, then the qualitative decision is based around price, valuation and sentiment. The extreme limits of these are easy to specify; expect OM to be well out of these names when you start seeing the companies trading at multiples of NAV, or read/hear about shipping companies as “high dividend names” or that shipping day rates will stay at elevated levels for years (i.e. the sector is no longer cyclical). Finally, Our Man is also watching to see when the names are added to different ETFs. While the stocks will certainly benefit from the wall of passive money flowing into them it’s a strong signal that the end is near for Shipping as a dislocation position in OM’s portfolio*.

Conclusion

Our Man hopes that the three points above – accepting that Shipping will be volatile (and will drive the portfolio’s short-term moves), remembering why he’s invested, and having a plan – will help him manage the shipping positions over the coming quarters. He’s also listed some of the fundamental and other qualitative factors he’s watching to try and help prevent thesis creep, so expect updates on these during the quarterly reviews. Finally, if you ever hear OM talking about how Shipping cos are high dividend names…then less than politely ask him what the hell he’s doing and remind him of this post!!

* For future reference, today the stocks are barely owned by ETFs – STNG (3.3% of market cap is held by ETFs), DSSI (2.5%) and EURN (2.1%). For comparison, large bell weather stocks (AAPL, GOOGL, FB, BA, GE, etc.) have ~10% of their market cap owned by ETFs and some stocks can have 40%+ of their market cap owned by passive investors.

Disclaimer: Nothing above represents a recommendation in any way, shape or form so please don’t even think of trying to take it that way. For added clarity, while Our Man is invested in STNG, DSSSI and EURN that’s a terrible reason for anyone else to invest in them. You should not buy any of these securities because Our Man has mentioned them, but should do your own work and decide what’s best for you given your own circumstances/risk tolerance/etc.

{kind=link}