Portfolio Update

As noted in the recent portfolio update, Our Man made several changes to the portfolio during the second half of April.

- Uranium: OM increased and consolidated the exposure, by adding to the Uranium Miners ETF (URNM) and the Uranium Junior Miners ETF (URNJ), while fully exiting the remaining single name positions (NXE and SMR).

- US Reindustrialization: OM remains confident that the market continues to underestimate the scale and impact of US reindustrialization. OM increased the position in the American Industrial Renaissance ETF (AIRR).

- Carbon: OM materially increased the position in California Carbon Allowances (KCCA) as prices traded near their floor.

- Commodities: A small position in Lundin Mining Corp (LUNMF) – inherited through the takeover of Filo Mining Group (FLMMF) - was modestly increased.

- European/UK Banks: Positions in Barclays Bank (BARC), Lloyds Banking Group (LYG) and Natwest Group (NWG) were all trimmed.

- Position Exits: OM fully exited several smaller holdings to reallocate capital towards higher conviction ideas. These included positions in Greece (ALBKY), Brazil (EWZ), and Biotech (IBB and XBI) and the Idiosyncratic Equity position in Texas Pacific Land (TPL).

Performance and Review

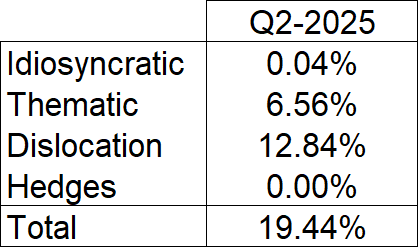

Our Man’s portfolio bounced back strongly during the second quarter, posting strong gains in each month and rising 19.4% during the quarter. This was comfortably ahead of the S&P 500 TR (+10.9%) and the MSCI World (+9.5%).

The portfolio’s Q2 gains saw it end the quarter at 12.0% YTD, which is comfortably ahead of the market (S&P 500 TR: +6.2% and MSCI World: +6.6%).

Second Quarter Attribution

As noted in the recent portfolio update, Our Man made several changes to the portfolio during the second half of April.

- Uranium: OM increased and consolidated the exposure, by adding to the Uranium Miners ETF (URNM) and the Uranium Junior Miners ETF (URNJ), while fully exiting the remaining single name positions (NXE and SMR).

- US Reindustrialization: OM remains confident that the market continues to underestimate the scale and impact of US reindustrialization. OM increased the position in the American Industrial Renaissance ETF (AIRR).

- Carbon: OM materially increased the position in California Carbon Allowances (KCCA) as prices traded near their floor.

- Commodities: A small position in Lundin Mining Corp (LUNMF) – inherited through the takeover of Filo Mining Group (FLMMF) - was modestly increased.

- European/UK Banks: Positions in Barclays Bank (BARC), Lloyds Banking Group (LYG) and Natwest Group (NWG) were all trimmed.

- Position Exits: OM fully exited several smaller holdings to reallocate capital towards higher conviction ideas. These included positions in Greece (ALBKY), Brazil (EWZ), and Biotech (IBB and XBI) and the Idiosyncratic Equity position in Texas Pacific Land (TPL).

Performance and Review

Our Man’s portfolio bounced back strongly during the second quarter, posting strong gains in each month and rising 19.4% during the quarter. This was comfortably ahead of the S&P 500 TR (+10.9%) and the MSCI World (+9.5%).

The portfolio’s Q2 gains saw it end the quarter at 12.0% YTD, which is comfortably ahead of the market (S&P 500 TR: +6.2% and MSCI World: +6.6%).

Second Quarter Attribution

While nearly all positions contributed positively, Q2 performance was driven primarily by the Uranium position (+1,107bps), which rallied just under 50% in the quarter. Truthfully, little new or special occurred in Q2 - OM simply benefited from having a well-sized position and the discipline to look through Q1s volatility. The position gained from several ongoing tailwinds:

Other major contributors: European/U.K. Financials (+298bps) and US Reindustrialization (+224bps) rallied after Q1 earnings exceeded expectations and forward guidance helped ease investor concerns. Tin (+158bps) surged in April after geopolitical risk around Alphamin’s Congo mine eased, following a U.S.-brokered settlement between DR Congo and Rwanda. The position also benefited from a strategic shift, with Alphamin’s largest shareholder agreeing to be bought out by Abu Dhabi–based International Resources Holding. Blockchain/Crypto (+110bps) was supported by expanding global liquidity and a post-halving price trend consistent with prior cycles. OM still expects to exit this theme during 2025.

The only significant detractor was Argentina (-128bps), which gave back a portion of its strong 2024 gains. While President Milei’s reforms are off to a solid start and are improving the macro outlook and buoying investor confidence, progress remains early. The upcoming October midterms will be a key test. Short-term sentiment was also dented after Argentina was not added to the MSCI Emerging Markets Index in June – a disappointment for some investors and a drag on local equity market performance.

The portfolio saw healthy performance from Shipping/Tankers (+66bps), India (+53bps), Carbon (+43bps), and Commodities (+30bps). Meanwhile, China (+1bp) and Idiosyncratic Equities (+4bps) had no material impact on performance. Positions that were exited during the quarter modestly detracted from performance – Greece (-11bps), Biotech (-17bps), and Brazil (+7bps) – though this capital was redeployed profitably elsewhere.

Portfolio (as at 06/30/25 - all delta and leverage adjusted, as appropriate)

Dislocations: 54.3%

28.0% - Uranium (URNM & URNJ)

12.4% - European/UK Financials (BCS, LYG, & NWG)

8.7% - Argentina (BMA, GGAL, & SUPV)

5.2% - China (KWEB, FXI & JD)

Thematic: 42.4%

11.7% - US Reindustrialization (AIRR)

9.2% - Carbon Credit Allowances (KCCA)

6.7% - Shipping/Tankers (STNG, INSW, TNK, DHT & FRO)

4.9% - India (IBN, INDA & SMIN)

4.8% - Tin (AFMJF, MLXEF & SBWFF)

3.9% - Blockchain/Crypto (IBIT, ETHE/ETH & OSTK)

1.2% - Commodities/Mining (LUNMF)

Idiosyncratic: 2.5%

2.5% - Equities (JOE)

Shorts/Hedges: 0.0%

Cash: 0.7%

Disclaimer: Nothing above represents a recommendation in any way, shape or form so please don’t even think of trying to take it that way. For added clarity, while Our Man is invested in all of the securities mentioned that’s a terrible reason for anyone else to do so. Our Man also holds some cash and a few other securities (of negligible value). You should not buy any of these securities because Our Man has mentioned them, but should do your own work and decide what’s best for you given your own circumstances/risk tolerance/etc.

- Data center demand for nuclear power: Tech hyperscalers continued efforts to secure nuclear energy for AI-driven data center growth—an initiative underway since 2023. Notable examples include Amazon’s $650M deal with Talen Energy (March 2024) and the planned reopening of Three Mile Island for Microsoft.

- Policy support: The Trump Administration has been vocal in its pro-nuclear stance, taking Q2 steps to streamline nuclear project approvals.

- Technical tailwinds: Strong inflows into the largest physical Uranium ETF further tightened the spot market.

Other major contributors: European/U.K. Financials (+298bps) and US Reindustrialization (+224bps) rallied after Q1 earnings exceeded expectations and forward guidance helped ease investor concerns. Tin (+158bps) surged in April after geopolitical risk around Alphamin’s Congo mine eased, following a U.S.-brokered settlement between DR Congo and Rwanda. The position also benefited from a strategic shift, with Alphamin’s largest shareholder agreeing to be bought out by Abu Dhabi–based International Resources Holding. Blockchain/Crypto (+110bps) was supported by expanding global liquidity and a post-halving price trend consistent with prior cycles. OM still expects to exit this theme during 2025.

The only significant detractor was Argentina (-128bps), which gave back a portion of its strong 2024 gains. While President Milei’s reforms are off to a solid start and are improving the macro outlook and buoying investor confidence, progress remains early. The upcoming October midterms will be a key test. Short-term sentiment was also dented after Argentina was not added to the MSCI Emerging Markets Index in June – a disappointment for some investors and a drag on local equity market performance.

The portfolio saw healthy performance from Shipping/Tankers (+66bps), India (+53bps), Carbon (+43bps), and Commodities (+30bps). Meanwhile, China (+1bp) and Idiosyncratic Equities (+4bps) had no material impact on performance. Positions that were exited during the quarter modestly detracted from performance – Greece (-11bps), Biotech (-17bps), and Brazil (+7bps) – though this capital was redeployed profitably elsewhere.

Portfolio (as at 06/30/25 - all delta and leverage adjusted, as appropriate)

Dislocations: 54.3%

28.0% - Uranium (URNM & URNJ)

12.4% - European/UK Financials (BCS, LYG, & NWG)

8.7% - Argentina (BMA, GGAL, & SUPV)

5.2% - China (KWEB, FXI & JD)

Thematic: 42.4%

11.7% - US Reindustrialization (AIRR)

9.2% - Carbon Credit Allowances (KCCA)

6.7% - Shipping/Tankers (STNG, INSW, TNK, DHT & FRO)

4.9% - India (IBN, INDA & SMIN)

4.8% - Tin (AFMJF, MLXEF & SBWFF)

3.9% - Blockchain/Crypto (IBIT, ETHE/ETH & OSTK)

1.2% - Commodities/Mining (LUNMF)

Idiosyncratic: 2.5%

2.5% - Equities (JOE)

Shorts/Hedges: 0.0%

Cash: 0.7%

Disclaimer: Nothing above represents a recommendation in any way, shape or form so please don’t even think of trying to take it that way. For added clarity, while Our Man is invested in all of the securities mentioned that’s a terrible reason for anyone else to do so. Our Man also holds some cash and a few other securities (of negligible value). You should not buy any of these securities because Our Man has mentioned them, but should do your own work and decide what’s best for you given your own circumstances/risk tolerance/etc.