No major updates from Our Man, though he's (still) working on a software (Enterprise, not Consumer) thesis. Instead, another edition of “Things from my Newsblur” - this time some recent(ish) articles that have caught OM's eye, but didn't get enough attention generally.

Live Long – What Really Extends Lifespan

This isn’t actually an article, but a graphic of the way various traits affect lifespan. The strength of the science is clearly shown, and ranges from suggestive to strong. The traits range from the subtle (drinking a little alcohol vs. abstinence) to the more obvious (avoid cancer). Well worth a look! (Dave McCandless, Information is Beautiful)

This 8-Year Old Chess Champion Will Make you Smile

While last week saw a college admissions scandal in the US, this heartwarming article is another little reminder that talent is universal but opportunity is not. (Nicolas Kristof, New York Times)

Into the Dark

The Thai cave rescue seemed crazy at the time. After reading Shannon Gormley’s article, based on months of in-person interviews with the key protagonists, it seems even crazier. The confluence of skill, meticulous planning and luck required not just by the dive-team but also by the support staff (and Thai government) is astouding. It’s the kind of story that if you read it in a book (or saw in a film) you wouldn’t believe. (Shannon Gormley, Macleans)

Humanity + AI = Better Together

Robots are coming for your jobs! Skynet is after your children! Really? Well, the flip side of the popular narrative is that in conjunction with AI - we will become more creative, improve our productivity and powers, make better decisions, be safer as dangerous tasks can be automated and understand each other better. Too good to be true? Well, Frank Chen takes us through those positive arguments. (Frank Chen, a16z)

Here’s why we’re entering the Golden Age of Podcasts

Our Man has been an avid podcast listener for many a year, and it seems that 2018 is the year they finally broke into the mainstream. Perhaps, the hit podcast Serial was the gateway drug for folks. This article shows the state of podcasts in 10 charts, with some thoughts on what’s next! (Dave Zohrob, Chartable Blog)

The Hunt for Planet Nine

Mike Brown is the “Pluto Killer”; a man with dozens of astronomical discoveries to his name, including the dwarf planets Sedna and Eris. Konstantin Batygin is a renowned theoretical astrophysicist, who at age 22 mathematically proved our universe is unstable (don’t worry, we’ve got a few thousand years before Mercury crashes into the sun, or Venus!). After analyzing historical data, they proposed in January 2016 that there was a giant planet orbiting far away from everything. The hunt is on to find “Planet Nine”, and this is their tale. (Shannon Stirone, Longreads)

Amazon’s Anti-trust Paradox

The history of anti-trust in the US is a surprisingly interesting topic, from its use to break-up Standard Oil in 1911 to its subsequent over-reach in the 1960’s and 1970’s, which saw Robert Bork redefine the term “competition” and paved the way for today’s University of Chicago inspired laissez faire approach. Lina Khan’s article, combined with the discussion around ‘Big Tech’, has perhaps paved the way for a new interpretation of anti-trust law. (Lina M. Khan, Yale Law Journal)

Sunday, March 24

Tuesday, March 5

Half-Baked Idea: Chinese A-Shares

[Quick thing: OM changed the provider that sends these emails out, so hopefully you’re all receiving this. I’d say holler if you’re not, but err…hopefully, the new ‘advanced’ software will let me know you’re not (or at least didn’t open this email) else this bit is all a bit moot!]

This is something OM has been pondering for a couple of months; though, he thought (and still thinks, even with the big move in A-Shares) that it would be a late 2019/early 2020 trade.

This idea is all about pattern recognition, backed up by a collection of circumstantial evidence so it will always be a more speculative idea. That doesn’t mean OM won’t take a position in it at some point, though it would likely be a 6-18mos trade and thus not a huge position.

The above is a long-term OEW technical chart of China. If you look at the lows (05/06, 08/09, 13/14, and now 18/19….even back to 94/95) – all down 50%+ from prior peak. All were followed by sharp rises in the following years. If history is a guide, or at least could rhyme a little, this C-wave should last ~2years and if the last few bull markets are anything to go by, the IRR could be spectacular. For comparison, post-06 the market was up 500% in ~2yrs, post-08/09 it more doubled in about a year, and after the 13/14 low it almost tripled by mid-2015. In the case of both post-06 and after the 13/14 lows, the rally started off slowly before going exponential towards the end.

So the technical perspective is that we potentially saw a new major low at the end of 2018. In the short term, MSCI’s recent announcement of mid-2019’s large increase in China’s weighting in the MSCI Emerging Market Index has helped the new bull market establish itself.

Given this good news, why does OM like the ~2 year time frame? Well, he rather suspects it fits well with the Communist Party’s incentives. Consider the following timeline:

- 2021 is the Centenary of the Communist Party of China's founding, marking the start of the “two centenary goals”*. The goals were put down in writing at the 18th National Congress (in 2012) when Xi Jinping became leader. Xi has subsequently linked them to the “Chinese dream”.

- 2022 sees the next National Congress where Xi likely to be the first leader to run for a 3rd term.

The Party has a strong incentive for China to go into those two events with a strong economy. That means using 2019 to sort out some of China’s imbalances - and the trade dispute with the US provides great cover/excuse for this, whether there a deal or no deal! This will prevent overheating when China stimulates and allows them to stimulate aggressively in 2020 to ensure a strong 2021-2022.

So now you know the half-baked idea, expect an update if OM is putting it into the book.

*The other centenary is that of the founding of the People’s Republic of China in 2049.

This is something OM has been pondering for a couple of months; though, he thought (and still thinks, even with the big move in A-Shares) that it would be a late 2019/early 2020 trade.

This idea is all about pattern recognition, backed up by a collection of circumstantial evidence so it will always be a more speculative idea. That doesn’t mean OM won’t take a position in it at some point, though it would likely be a 6-18mos trade and thus not a huge position.

The above is a long-term OEW technical chart of China. If you look at the lows (05/06, 08/09, 13/14, and now 18/19….even back to 94/95) – all down 50%+ from prior peak. All were followed by sharp rises in the following years. If history is a guide, or at least could rhyme a little, this C-wave should last ~2years and if the last few bull markets are anything to go by, the IRR could be spectacular. For comparison, post-06 the market was up 500% in ~2yrs, post-08/09 it more doubled in about a year, and after the 13/14 low it almost tripled by mid-2015. In the case of both post-06 and after the 13/14 lows, the rally started off slowly before going exponential towards the end.

So the technical perspective is that we potentially saw a new major low at the end of 2018. In the short term, MSCI’s recent announcement of mid-2019’s large increase in China’s weighting in the MSCI Emerging Market Index has helped the new bull market establish itself.

Given this good news, why does OM like the ~2 year time frame? Well, he rather suspects it fits well with the Communist Party’s incentives. Consider the following timeline:

- 2021 is the Centenary of the Communist Party of China's founding, marking the start of the “two centenary goals”*. The goals were put down in writing at the 18th National Congress (in 2012) when Xi Jinping became leader. Xi has subsequently linked them to the “Chinese dream”.

- 2022 sees the next National Congress where Xi likely to be the first leader to run for a 3rd term.

The Party has a strong incentive for China to go into those two events with a strong economy. That means using 2019 to sort out some of China’s imbalances - and the trade dispute with the US provides great cover/excuse for this, whether there a deal or no deal! This will prevent overheating when China stimulates and allows them to stimulate aggressively in 2020 to ensure a strong 2021-2022.

So now you know the half-baked idea, expect an update if OM is putting it into the book.

*The other centenary is that of the founding of the People’s Republic of China in 2049.

Friday, February 1

Half (Well Almost Entirely) Baked Ideas: Dislocation - Shipping

Folks who know Our Man will have heard him talk about this idea at various points over the last 6-9 months. He’s been quietly working away on it and it’s close to going into the portfolio, which I guess makes this a nearly fully-baked idea! Hopefully, the half-baked series means that ideas like this will be shared earlier in the process!

The Shipping sector does not have a good reputation in the investor community, having burned most who have invested there and largely ignored by the rest. What’s the deal?

It is one of the only places where prices are still way below 2008. For example, here’s the chart for Frontline, one of the world’s largest oil tanker shipping companies. Yup, it trades at ~$5, having been over $200 before the Financial Crisis.

However, the poor performance since the crisis is for good reasons.

- Over-Supply: The run-up in prices leading into 2008 led to massive oversupply and low rates since has helped perpetuate it. As ships have 20-25 year-lives, it takes a LONG time to work it off that over-supply!

- Trade War: 70% of global trade is done via shipping, so the sector doubly out of favor at the moment

- Operational leverage & Incentives: Most of the industry’s costs are fixed (buying/building a ship) and the operational costs are relatively low, which means that there is huge operating leverage. In good times, this sees revenue drop quickly to the bottom line and profits can rise sharply but in bad times the opposite happens. What’s worse is that ship-operators have an incentive to show no price discipline in those bad times, i.e. they set price to cover only their operational costs.

- Financial leverage: To further increase the volatility, most operators are financially levered (both directly and indirectly). Ironically, despite the leverage leading to bankruptcies it does not benefit the strong players as firms go through pre-packaged Chapter 11’s rather than having to sell ships at a big discount.

The combination of the last two is why many investors hate shipping, when it goes wrong it goes spectacularly wrong very quickly!!

However, there are some strong signs that Shipping may fit OM’s Dislocation paradigm!

i) Reaction: Your reaction to this is probably “mate, really…are you crazy?”

ii). Value/Cheap: It’s now old fashioned value/cheap; the companies are trading at or substantially below book value.

iii). Narrative: Finally, this is about to change due a major regulatory initiative - IMO 2020 – that goes into effect on January 1st, 2020.

- What is IMO 2020? Well, it’s a new regulatory regime that prohibits vessels from using high-sulfur fuel oil (HSFO) unless they can capture the pollution causing materials. The allowed sulfur content is falling dramatically from 3.5% to 0.5%.

- There is no ease-in or adjustment period. Jan 1st, 2020 is the drop-dead date for compliance.

- Ship operators have 3 choices: Use low-sulfur marine gas oil (MGO), retrofit their ships to use liquefied natural gas or install scrubbers (to capture the pollution causing materials).

- Scrubbers are a popular choice but are expensive ($1-10mn/ship) and no panacea (diluting pollutants and dumping in ocean vs. into air). Given the congestion in major shipping lanes (Singapore, English Channel, in the Gulf of Mexico, etc.) this means that certain ports (including the world’s largest, Singapore) are already banning the use of open-loop scrubbers. This reduces the cost effectiveness of scrubbers, though their ‘apparent’ effectiveness is already debatable*.

Created by London-based data visualisation

studio Kiln and the UCL Energy

Institute

- Given the costs of the various options for IMO 2020 compliance a number of older ships are expected to be retired, reducing the supply of vessels.

So, how to take advantage of all these changes?

Here are a few things that OM has drawn from the above:

- Size matters. The bigger firms have more flexibility, be it the ability to pass on costs to clients or just in waiting to see how the port-related risks with scrubbers plays out.

- In many ways IMO 2020 isn’t a shipping debate, but an oil production/refining one; there is now a price on sulfur content in oil, and this will create dislocations and arbitrages in that market.

One of the biggest disruptions will be in the high-sulphur fuel oil (HSFO); HSFO fuel was often created by mixing very high sulfur and very low sulfur oils. Will this still be the best economic choice or will refiners change their feedstocks and choose not to make HSFO?

Why mention this? Because it matters for oil tankers (as opposed to dry cargo, cruise ships, etc.) as they carry oil, and oil routes are about to change depending on the new refining needs. For example, US Gulf Coast refiners currently don’t crack high sulfur oil as it is uneconomical. Instead they use shale oil, which comes at a discount. How does this change in 2020 if/when shale oil becomes more expensive as increased pipeline capacity comes online removing the discount and the price of high-sulfur oil falls.

What does all this mean for Our Man’s portfolio?

It’s going to focus on companies with large fleets that move oil or finished petroleum products!

Specifically, he’s starting with Scorpio Tankers (STNG, leading transported of refined petroleum products) and EuroNav (EURN, largest independent listed oil tanker company). He’s also looking at Navigator Holdings (NVGS, largest fleet of liquefied natural gas carriers).

------------------------------------------------------------------------------------------

Side Note:

* Economically, scrubbers actually add to the industry’s incentive problems. Scrubbers are paid for up front, with shippers ‘benefiting’ from the lower price of HFSO fuel to ‘earn’ it back. This adds to the operating leverage (more fixed costs) and there are clear issues with this:

(i) Unless freight prices are based on the more expensive low sulfur fuel (MGO), the shipper is worse off vs. pre-IMO 2020 (it pays the capex, but fuel costs and pricing stay the same)

(ii) Will the spread between MGO and HSFO fuel remain the same?

This isn’t known yet; people are assuming it will but we can look at some history as a guide;

- Shipping moved to tighten Emission Control Areas (ECAs) - where stricter controls were used to minimize airborne emissions – from 1.0% to 0.1% in 2015. Part of the assumption and expectation was that the fuel spread would compensate shippers. It did not, the spread collapsed along with the oil price in 2015.

(ii) Finally, will there be a change in regulations (or a veto of scrubbers by major ports) that changes the payback period or makes the capex wasted. While this sounds crazy, there is precedent here.

- Following the Exxon Valdez disaster, the IMO mandated the move from single-hull tankers to double hull tankers. The IMO date for obsolescence of single hull tankers was 2015, yet there were almost no single hulls afloat after 2007! Why? The oil majors just wouldn’t contract them. Incidentally, this was a major boon to stock prices for the well positioned companies (see FRO chart above, I’ll wait. Yeah, it went from ~$2.5 to ~$280 in ~5yrs…and it’s almost come all the way back down; that is shipping!)

Now bring it forward to today, Singapore is the world’s largest port, and is known for being very commercial. Do you think they didn’t consult any of the other major ports and acted alone when unilaterally banning scrubbers in their water?

So, take it with a large grain of salt if you hear someone telling you scrubbers are the perfect solution to IMO 2020!

Sunday, January 20

Things from my Newsblur; 2019 Part I

Let’s begin this year as we mean to go on, with an early edition of “Things from my Newsblur”. As usual, the most investment-related stuff is at the end.

Dwarf planet 'The Goblin' discovery redefining solar system

Approaching Halloween last year, one of Our Man’s son’s was very into space and especially the hypothetical Planet 9 and the Dwarf planets. Imagine the joy, at (i) the discovery of a new dwarf planet, (ii) that it’s called ‘The Goblin’, and (iii) that its existence and orbit further suggest Planet 9 is out there. Happy days, though the song needs updating!

(Hannah Devlin, The Guardian)

Women’s Pockets are Inferior

Mrs. OM hcompains about the frustration of women’s pockets, and especially the decorative faux pockets. Well, here’s the data (and cool graphics) on the differences in pocket sizes and shapes in twenty of the most popular blue jeans for men and women. Spoiler alert: No shock but the data proves that women have a right to be upset!

(Jan Diehm & Amber Thomas, Pudding.cool)

Rodney Brooks: Tech Prediction Scorecard, January 2019

Predicting the future is fraught with the risk of looking foolish…and more so when you’re looking at to 2050 and thinking about technological change. A year ago, Rodney Brooks made multiple predictions on self-driving cars, artificial intelligence and machine learning, and the space industry. He will revisit them and highlight the progress, as well as where he is on track or off base. If you only read one blog post on those subjects, each year, make it this one.

Why is it interesting? Well, the future is interesting, and Dr. Brooks is more qualified than most to hazard these guesses. Additionally, we can see how the data and his thinking evolve each year - process matters! Dr. Brooks is the Panasonic Professor of Robotics at MIT, where he was also the Director of the MIT Artificial Intelligence Lab. He’s also a Founder, former Board Member and former CTO of iRobot.

(Rodney Brooks, his blog).

Vietnam is Winning the US-China Trade War

With the current US-China trade war picking up, and the sense that it’s the start of a new dynamic between the two countries rather than a one-off spat, technology manufacturers are starting to set-up factories elsewhere. This coupled with Vietnam opening up to free trade (e.g. the TPP and a trade deal with Europe) has meant that “Vietnam, once dependent on garments and other cheap exports, has begun to rival China’s tech sector.” This is not something new, but merely Vietnam starting to tread down the path that Thailand took ~30yrs ago, and China ~20-25yrs ago. Absent a major change, expect Vietnam to be Our Man’s portfolio for a looooooong time!

(Bennett Murray, Foreign Policy)

Dwarf planet 'The Goblin' discovery redefining solar system

Approaching Halloween last year, one of Our Man’s son’s was very into space and especially the hypothetical Planet 9 and the Dwarf planets. Imagine the joy, at (i) the discovery of a new dwarf planet, (ii) that it’s called ‘The Goblin’, and (iii) that its existence and orbit further suggest Planet 9 is out there. Happy days, though the song needs updating!

(Hannah Devlin, The Guardian)

Women’s Pockets are Inferior

Mrs. OM hcompains about the frustration of women’s pockets, and especially the decorative faux pockets. Well, here’s the data (and cool graphics) on the differences in pocket sizes and shapes in twenty of the most popular blue jeans for men and women. Spoiler alert: No shock but the data proves that women have a right to be upset!

(Jan Diehm & Amber Thomas, Pudding.cool)

Rodney Brooks: Tech Prediction Scorecard, January 2019

Predicting the future is fraught with the risk of looking foolish…and more so when you’re looking at to 2050 and thinking about technological change. A year ago, Rodney Brooks made multiple predictions on self-driving cars, artificial intelligence and machine learning, and the space industry. He will revisit them and highlight the progress, as well as where he is on track or off base. If you only read one blog post on those subjects, each year, make it this one.

Why is it interesting? Well, the future is interesting, and Dr. Brooks is more qualified than most to hazard these guesses. Additionally, we can see how the data and his thinking evolve each year - process matters! Dr. Brooks is the Panasonic Professor of Robotics at MIT, where he was also the Director of the MIT Artificial Intelligence Lab. He’s also a Founder, former Board Member and former CTO of iRobot.

(Rodney Brooks, his blog).

Vietnam is Winning the US-China Trade War

With the current US-China trade war picking up, and the sense that it’s the start of a new dynamic between the two countries rather than a one-off spat, technology manufacturers are starting to set-up factories elsewhere. This coupled with Vietnam opening up to free trade (e.g. the TPP and a trade deal with Europe) has meant that “Vietnam, once dependent on garments and other cheap exports, has begun to rival China’s tech sector.” This is not something new, but merely Vietnam starting to tread down the path that Thailand took ~30yrs ago, and China ~20-25yrs ago. Absent a major change, expect Vietnam to be Our Man’s portfolio for a looooooong time!

(Bennett Murray, Foreign Policy)

How Open-Source Software Took Over the World

Regular readers will know that OM has been reading about, linking to, and mentioning software (especially enterprise) a lot recently. Five years ago, the idea that open-source software was viable let alone would be dominant was met with skepticism from investors. The world has certainly changed, with IBM’s purchase of Redhat (for $32 billion!!) headlining a list of multi-billion dollar takeovers, IPOs and companies! Mike Volpi goes through the evolution of open-source software from Linux and MySQL, through the second generation and how it evolved towards Software-as-a-Service business models enabled by the cloud.

(Mike Volpi, TechCrunch)

But…

AWS, MongoDB, and the Economic Realities of Open Source

What if enterprise open-source software is music; and the software cos are the record cos? Music like open-source software is relatively worthless once it’s been produced, since it can be copied endlessly. Record companies don’t sell music, but rather the tools that make music usable (i.e. CDs in the good ole days)…and it is the same with open-source software, especially in the cloud era. Therein lies the rub, will the value accrue to software cos (or record companies) or to those companies (and products) like Amazon Web Services, Microsoft's Azure, etc. (or Spotify, Apple Music, etc in the case of music) that provide the convenience to the end customer.

(Ben Thomspon, Stratechery – if you like technology and read nobody else on a weekly basis, read Ben!).

Tuesday, January 15

2018: Fourth Quarter Review

Portfolio Update

Our Man’s working view is that things are okay despite the market’s gyrations and what you might have read. While there is much uncertainty, the probability of a recession or credit market crunch currently remains low. Markets have just moved from pricing in a scenario where everything goes perfectly, to one which suitably acknowledges the uncertainties. Our Man expects that the market may retest the December lows, or at least see a meaningful pullback when this rally ends, and he will look to continue buying during that move.

What’s he looking to add to the portfolio?

It will be a barbell approach; either positions where there is an event or catalyst in the coming year that will focus investors’ attention, or where the long-term secular trend is understood yet the current price provides a decent entry point for a multi-year holding. OM also expects to re-enter the Technical book’s position, once he receives the requisite buy-signal.

Looking back at the 4th quarter, the changes to the portfolio occurred in three distinct phases:

- The first set of trades, in early-to-mid October were largely discussed in prior posts. Our Man added to his Vietnam position (VNM) and exited the Technical Book (SSO, QLD and DDM), further reduced the idiosyncratic TPL position and trimmed his Brazil exposure (EWZ and EWZS). Later in the month, he also went from long biotech (IBB) to short biotech (BIS).

- At the end of November, Our Man started a new Theme-Blockchain position, with a position in Overstock (OSTK).

- In the second half of December, Our Man added materially to the Dislocation-Greece position through the existing positions in the Greece ETF (GREK) and Alpha Bank (ALBKY), as well as a new position in Eurobank (EFGEY). This recent piece from the last “Things from my Newsblur”, offers a detailed look at Greece (and especially Eurobank). Our Man will write more but in essence; valuation is now reaching an absolute extreme, investor sentiment is terrible and has significantly diverged from fundamentals, but there is also a catalyst (elections!) in 2019 that can change that sentiment.

Performance and Review

The final quarter saw the portfolio fall -5.7%, which was substantially better than the S&P 500 Total Return (-13.5%) and the MSCI World (Net Dividends) (-13.4%). Unsurprisingly, the majority of OM’s negative performance (-3.24%) came in the first 11 days of October before any of the changes were made to the portfolio.

Overall, Our Man’s October assertion that the portfolio changes had likely locked in 2018’s performance between -5% and -15% just about held true; the portfolio’s YTD performance ended at -14.9%. Disappointingly this trailed both S&P 500 Total Return (-4.3%) and the MSCI World (ND) (-8.7%) by a material amount – though the damage was done early in 2018.

There were very few surprises in the portfolio’s performance during the 4th quarter, as it held-up consistently well and Brazil’s strength prevented any negative skew from developing.

Dislocations

- Brazil was a major contributor, adding 268bps to performance, following Bolsonaro’s win in the Presidential elections. Our Man took advantage of the strong rise during October to significantly reduce the position. Brazil remains attractive and while a Bolsanaro presidency will likely help economically, unlike Greece and Argentina a change of government wasn’t part of OM’s thesis. As such, with reduced certainty and conviction, the position is smaller.

- Greece cost 141bps in the quarter. As noted, the discrepancy between OM perception of reality and investor sentiment/the market’s belief is now significant. If the technical picture was just a little better, OM would be all in.

- Uranium cost 122bps, as the stocks fell with equity markets. The last 15 months have seen numerous positive fundamental developments, especially the actions by Cameco & Kazatomprom to reduce supply, but no reaction from stock prices. The fourth quarter was similar with Uranium spot prices finally started to pick up (and long-term contract prices bottoming out) and Kazatomprom IPO’ing. If these can’t encourage investors to relook at the space over the next few months, and drive stock prices higher then Our Man really shouldn’t be here (and certainly not in this size).

Thematic

Argentina (-6bps) and India (0bps) were flat for the quarter, while Vietnam (-25bps) saw only a minimal loss. Argentina remains the most intriguing situation in the portfolio but it’s heavily dependent on whether President Macri runs again (and wins). Our Man can see a scenario where Argentina is down 50% this year, but also one where it’s the equivalent of buying US stocks in 1984! OM suspects you’ll see much discussion here about it over the course of the year…

While the above positions held up well, the same could not be said for the Tech: 4th Industrial Revolution (-97bps) and Blockchain (-69bps) themes, which both fell heavily. The technology positions are both Chinese so suffered with both the retreat in Technology names and the weakness in China. As for the Blockchain position; Our Man received a sympathetic “Investing is hard” email from a friend after Overstock announced a delay in the GSR deal within a week of OM’s post. They did not execute well!

Other

The Technical (-130bps in Q4) book was reduced in late September following an initial sell signal, but still suffered during the market’s pullback in early October. The pullback triggered the second sell signal, and the Technical positions were liquidated preventing any further loss. This meant that the technical book proved a healthy contributor for 2018.

The Idiosyncratic book’s losses (-307bps in Q4) were evenly split between the Funds book (-155bps) and the Equities (-152bps). Though Funds book fell, it managed to out-perform the market in the quarter. Despite being cutback (twice), Texas Pacific Land Trust (TPL) still cost 147bps. The company predominantly earns its revenue through royalties/leases for oil and gas production and easements (e.g. for oil pipes), largely in the Permian Basin. The stock suffered as the oil price collapsed during the quarter; though the medium-term impact on production (if any) will prove more meaningful for TPL.

Portfolio (as at 12/31/18 - all delta and leverage adjusted, as appropriate)

Dislocations: 28.2%

12.2% - Greece (GREK, ALBKY, EGFEY)

9.1% - Uranium (URA, and NXE)

6.9% - Brazil (EWZ)

Thematic: 22.0%

6.8% - Argentina (PAM, DESP, and AGRO)

6.0% - Vietnam (VNM)

4.5% - Tech: 4th Industrial Revolution (JD and VIPS)

2.7% - India (IFN)

2.1% - Blockchain

Idiosyncratic: 13.2%

10.8% - Funds (CWS, GVAL, and CAPE)

2.4% - Equities (TPL and FNMA)

Shorts/Hedges: -14.0%

-14.0 – Short Biotech (BIS)

Technical: 0.0%

Cash: 29.6%

Disclaimer: Nothing above represents a recommendation in any way, shape or form so please don’t even think of trying to take the above that way. For added clarity, while Our Man is invested in all of the securities mentioned that’s a terrible reason for anyone else to do so. Our Man also holds some cash and a few other securities (of negligible value). You should not buy any of these securities because Our Man has mentioned them, but should do your own work and decide what’s best for you given your own circumstances/risk tolerance/etc.

Wednesday, December 12

Portfolio Update: New Theme – Blockchain

Our Man can hear y’all shouting “Don’t do it” at him!!!

This piece started out just over a month ago, as a half-baked idea, but the collapse in cryptocurrency prices and a unique stock-specific situation meant OM did some more work and has started a blockchain theme. As such, this piece is now much longer than originally intended.

Some Scary Finance Terms Made Simpler

Before we dive into the blockchain, a side note on binaries, loss aversion, agency risk/problem, optionality and convexity. Those of us in finance throw around these terms which sound complex but really cover simple concepts.

Most public market investors avoid binary situations – ones where the probabilistic outcomes are bimodal and split, or in plain English where the result it likely either terrible or awesome with very little in between. The most common example is a single drug biotech company where the drug trial result is the difference between commercializing a multi-billion blockbuster drug and losing everything. This avoidance of binaries is not an irrational decision but reflects the traits of as loss aversion and the agency problem. Research has found that the pain of losing a dollar is vastly greater than the joy of making one, and so people understandably seek to avoid that loss, hence “loss aversion”. The agency problem arises since investors are largely managing other people’s money, which influences their decision making. What do I mean? Do you want to go to your boss with an idea that will lose everything if you’re wrong? Do you want to sit with clients and say we lost X% last quarter due to this one position, but that’s okay we knew there was a 40-50% chance of that happening? For almost all, the answer is no… they would invest their money in that idea but they won’t invest client money.

While this avoidance of binaries is a facet of public market investing, this is not the case elsewhere. Studies suggest up to 40% of venture-funded businesses fail and a similar number don’t generate the targeted returns, yet venture capital is a thriving industry. The reason is convexity; an investment is convex if the payoff is unbalanced for equally opposite outcomes – for example, if you can make 10 on that hypothetical drug being a success, while only losing 1 if it fails. It’s why venture capitalists focus on metrics like Total Addressable Market (TAM) for their start-ups – it helps to frame the company’s potential size, and is a proxy for the investment’s convexity. OM uses optionality to express the same concept, just with an acknowledgement that if he’s wrong the downside is losing the capital invested in the position (i.e. like an option!).

Crypto/Blockchain as Optionality

OM is fascinated by blockchain (and yes, cryptocurrencies) but as friends know, is exceptionally reticent to talk about anything to do with investing in it. It’s so early in its lifecycle that any investments are akin to venture capital – it’s almost impossible to accurately value and there’s a significant probability you will lose your money. Thus OM’s sole advice is do your homework and invest as much as you’re willing to mentally write off not matter how fascinating and misunderstood it is.

With that said, OM is going to share just a little of his thinking on the blockchain as its convexity is part of the thesis. However, to avoid diving down rabbit holes, the following should be considered a gross simplification (some links are embedded for those who want to dig deeper).

There are two broad views of blockchain technology (and the related cryptocurrencies).

1. It will disrupt the Federal Reserve and/or become a store of value/money. That’s cool, and could be very valuable, but frankly OM isn’t really that interested in it. Yes, bitcoin *could* become a mix of digital gold and “money” and there will be profits to be made as in that journey, but it’s not for OM.

2. The potential for creating Web 3.0. This came to life with the creation of Ethereum and is what fascinates OM.

• Web 1.0 was the Internet of OM’s young adulthood (the 90s and early noughties, baby!!), where anyone could start a website as services were built on open internet protocols (points to the https at the start of website addresses, or the smtp protocol that allowed this email to reach you) that were ‘controlled’ by the Internet community.

• Web 2.0 is the Internet as we know it over the last 10-15 years, where major software companies have become centralized hubs of data and information. The historical resolution that occurs whenever an industry sees this type of extreme centralization, aka a monopoly, has been regulation.

• Web 3.0 could be the return of decentralization through blockchains, which use consensus mechanisms and cryptocurrencies to better align incentives. OM will spare you all the long explanations, but heartily recommends reading this piece (and everything else) by Chris Dixon.

The arguments for Web 3.0 are manifold but two that intrigue Our Man are:

(i) That you can build more advanced protocols – they’re decentralized and have fixed rules (like Web 1.0), but with greater functionality and better aligned incentives.

(ii) USV’s Fat Protocol Thesis. In Web 1.0 working groups and non-profits created protocols that produced massive value, which was predominantly captured by the applications (e.g. Google, Facebook, etc.). In the blockchain, this is reversed with the value flowing to the protocols (and, if well structured, their cryptocurrencies) rather than the applications built on top of them.

To be clear, it will take a long time. Progress will definitely not be linear and it is far from obvious which protocols and blockchains will ‘win’. However, if – and it is a huge if – blockchains do help engender Web 3.0 and we start to see applications that are native to blockchain (rather than mere copies of what exists elsewhere today), then the related protocols/blockchains will be worth substantially more than they are today. This is the type of convexity that intrigues OM and is drawing software engineers and venture capitalists into the industry.

So what does OM own?

Overstock (OSTK)! The crappy e-commerce stock, what does that have to do with Blockchain?

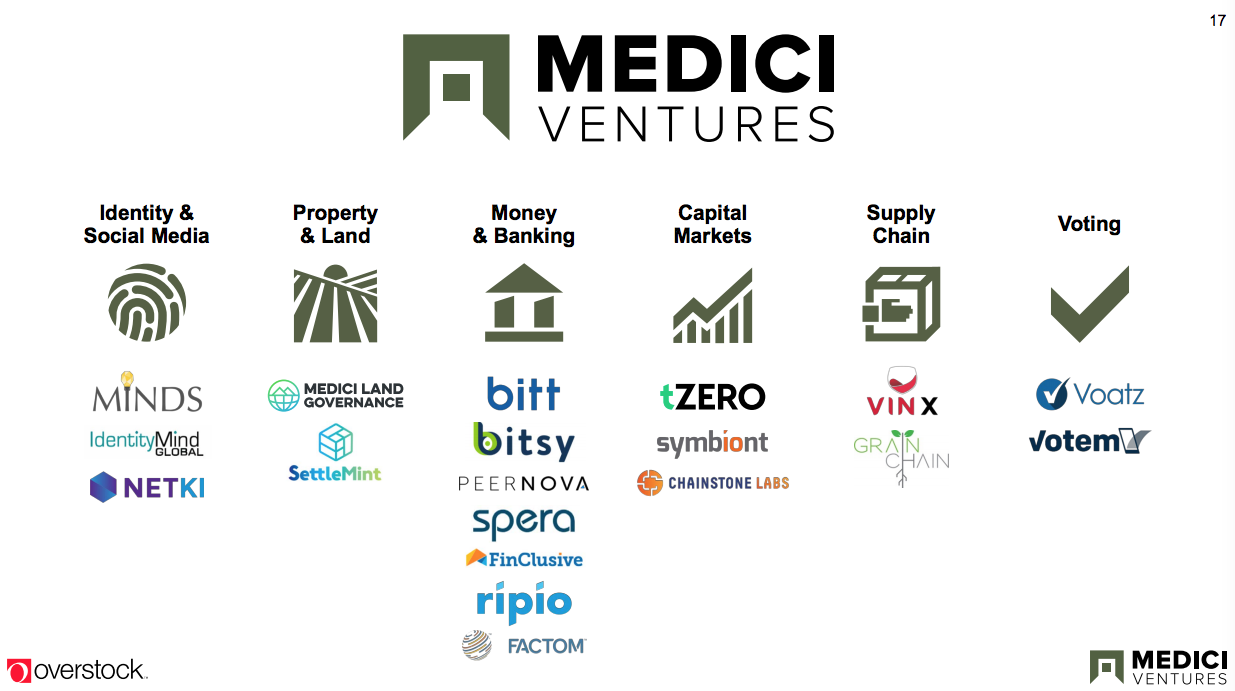

Well, largely unknown to most OSTK has slowly been turning itself into a blockchain VC firm. Four years ago, Overstock was the first retailer to accept bitcoin and over the last 4-years it has been putting capital into blockchain technology through its Medici Ventures subsidiary. Medici has invested in a dozen start-ups focused on six areas of blockchain adoption; capital markets, money and banking, property, voting and underlying technologies supporting blockchain.

The price over the last 18 months has started to reflect this transformation

This piece started out just over a month ago, as a half-baked idea, but the collapse in cryptocurrency prices and a unique stock-specific situation meant OM did some more work and has started a blockchain theme. As such, this piece is now much longer than originally intended.

Some Scary Finance Terms Made Simpler

Before we dive into the blockchain, a side note on binaries, loss aversion, agency risk/problem, optionality and convexity. Those of us in finance throw around these terms which sound complex but really cover simple concepts.

Most public market investors avoid binary situations – ones where the probabilistic outcomes are bimodal and split, or in plain English where the result it likely either terrible or awesome with very little in between. The most common example is a single drug biotech company where the drug trial result is the difference between commercializing a multi-billion blockbuster drug and losing everything. This avoidance of binaries is not an irrational decision but reflects the traits of as loss aversion and the agency problem. Research has found that the pain of losing a dollar is vastly greater than the joy of making one, and so people understandably seek to avoid that loss, hence “loss aversion”. The agency problem arises since investors are largely managing other people’s money, which influences their decision making. What do I mean? Do you want to go to your boss with an idea that will lose everything if you’re wrong? Do you want to sit with clients and say we lost X% last quarter due to this one position, but that’s okay we knew there was a 40-50% chance of that happening? For almost all, the answer is no… they would invest their money in that idea but they won’t invest client money.

While this avoidance of binaries is a facet of public market investing, this is not the case elsewhere. Studies suggest up to 40% of venture-funded businesses fail and a similar number don’t generate the targeted returns, yet venture capital is a thriving industry. The reason is convexity; an investment is convex if the payoff is unbalanced for equally opposite outcomes – for example, if you can make 10 on that hypothetical drug being a success, while only losing 1 if it fails. It’s why venture capitalists focus on metrics like Total Addressable Market (TAM) for their start-ups – it helps to frame the company’s potential size, and is a proxy for the investment’s convexity. OM uses optionality to express the same concept, just with an acknowledgement that if he’s wrong the downside is losing the capital invested in the position (i.e. like an option!).

Crypto/Blockchain as Optionality

OM is fascinated by blockchain (and yes, cryptocurrencies) but as friends know, is exceptionally reticent to talk about anything to do with investing in it. It’s so early in its lifecycle that any investments are akin to venture capital – it’s almost impossible to accurately value and there’s a significant probability you will lose your money. Thus OM’s sole advice is do your homework and invest as much as you’re willing to mentally write off not matter how fascinating and misunderstood it is.

With that said, OM is going to share just a little of his thinking on the blockchain as its convexity is part of the thesis. However, to avoid diving down rabbit holes, the following should be considered a gross simplification (some links are embedded for those who want to dig deeper).

There are two broad views of blockchain technology (and the related cryptocurrencies).

1. It will disrupt the Federal Reserve and/or become a store of value/money. That’s cool, and could be very valuable, but frankly OM isn’t really that interested in it. Yes, bitcoin *could* become a mix of digital gold and “money” and there will be profits to be made as in that journey, but it’s not for OM.

2. The potential for creating Web 3.0. This came to life with the creation of Ethereum and is what fascinates OM.

• Web 1.0 was the Internet of OM’s young adulthood (the 90s and early noughties, baby!!), where anyone could start a website as services were built on open internet protocols (points to the https at the start of website addresses, or the smtp protocol that allowed this email to reach you) that were ‘controlled’ by the Internet community.

• Web 2.0 is the Internet as we know it over the last 10-15 years, where major software companies have become centralized hubs of data and information. The historical resolution that occurs whenever an industry sees this type of extreme centralization, aka a monopoly, has been regulation.

• Web 3.0 could be the return of decentralization through blockchains, which use consensus mechanisms and cryptocurrencies to better align incentives. OM will spare you all the long explanations, but heartily recommends reading this piece (and everything else) by Chris Dixon.

The arguments for Web 3.0 are manifold but two that intrigue Our Man are:

(i) That you can build more advanced protocols – they’re decentralized and have fixed rules (like Web 1.0), but with greater functionality and better aligned incentives.

(ii) USV’s Fat Protocol Thesis. In Web 1.0 working groups and non-profits created protocols that produced massive value, which was predominantly captured by the applications (e.g. Google, Facebook, etc.). In the blockchain, this is reversed with the value flowing to the protocols (and, if well structured, their cryptocurrencies) rather than the applications built on top of them.

To be clear, it will take a long time. Progress will definitely not be linear and it is far from obvious which protocols and blockchains will ‘win’. However, if – and it is a huge if – blockchains do help engender Web 3.0 and we start to see applications that are native to blockchain (rather than mere copies of what exists elsewhere today), then the related protocols/blockchains will be worth substantially more than they are today. This is the type of convexity that intrigues OM and is drawing software engineers and venture capitalists into the industry.

So what does OM own?

Overstock (OSTK)! The crappy e-commerce stock, what does that have to do with Blockchain?

Well, largely unknown to most OSTK has slowly been turning itself into a blockchain VC firm. Four years ago, Overstock was the first retailer to accept bitcoin and over the last 4-years it has been putting capital into blockchain technology through its Medici Ventures subsidiary. Medici has invested in a dozen start-ups focused on six areas of blockchain adoption; capital markets, money and banking, property, voting and underlying technologies supporting blockchain.

The price over the last 18 months has started to reflect this transformation

So, why invest?

Convexity, of course! In addition to the convexity in the entire blockchain theme, discussed above, the collection of circumstances around Overstock has created meaningful convexity in the stock.

Some facts and figures on Overstock; it’s a ~$550mn market capitalization company with ~$180mn in cash on its balance sheet with no debt (~$3mn) and very limited liabilities. Patrick Byrne, the CEO, is exceptionally controversial with opinions running the gamut from genius to insane. He’s also a “true believer” in blockchain technology, with Overstock being the first retailer to accept bitcoin back in 2014. Finally, as noted it has two businesses; the online retail one that you likely recognize, and the blockchain venture capital one.

Retail Business

- The big news in November was that Overstock announced it was looking to sell its retail business in 2019.

- The retail business is a $1.8bn revenue business that has been slightly loss-making over the last decade, though losses accelerated in early 2018 before tempering.

- Since announcing it was looking to sell its retail business, Wall Street’s analyst’s valuation ranges on the business have been between $400mn and $1bn+. Our Man suspects the top-end is unrealistic; Overstock has never traded at the kind of valuation offered to similar e-commerce businesses (e.g. Wayfair). However, astute readers will note that even the low-end means that you get the blockchain business for free.

- The key will be execution, Overstock selling the business and for a decent price.

Blockchain Business

- Overstock’s blockchain business is through its wholly-owned subsidiary, Medici Ventures, a blockchain VC company.

- Overstock has invested $175mn in blockchain ventures through Medici, and its holdings can be seen below.

Convexity, of course! In addition to the convexity in the entire blockchain theme, discussed above, the collection of circumstances around Overstock has created meaningful convexity in the stock.

Some facts and figures on Overstock; it’s a ~$550mn market capitalization company with ~$180mn in cash on its balance sheet with no debt (~$3mn) and very limited liabilities. Patrick Byrne, the CEO, is exceptionally controversial with opinions running the gamut from genius to insane. He’s also a “true believer” in blockchain technology, with Overstock being the first retailer to accept bitcoin back in 2014. Finally, as noted it has two businesses; the online retail one that you likely recognize, and the blockchain venture capital one.

Retail Business

- The big news in November was that Overstock announced it was looking to sell its retail business in 2019.

- The retail business is a $1.8bn revenue business that has been slightly loss-making over the last decade, though losses accelerated in early 2018 before tempering.

- Since announcing it was looking to sell its retail business, Wall Street’s analyst’s valuation ranges on the business have been between $400mn and $1bn+. Our Man suspects the top-end is unrealistic; Overstock has never traded at the kind of valuation offered to similar e-commerce businesses (e.g. Wayfair). However, astute readers will note that even the low-end means that you get the blockchain business for free.

- The key will be execution, Overstock selling the business and for a decent price.

Blockchain Business

- Overstock’s blockchain business is through its wholly-owned subsidiary, Medici Ventures, a blockchain VC company.

- Overstock has invested $175mn in blockchain ventures through Medici, and its holdings can be seen below.

- The most promising Medici asset is tZero, which is an alternative trading system. Initially, it’s looking to transform the trading in ICOs, by making them compliant with SEC and FINRA regulations.

- Overstock is in talks with GSR (a Chinese PE firm) who completed their legal due diligence in Q3. The deal involves taking a stake in tZero equity and a purchase of Overstock equity, in addition to GSR’s position in the recently completed tZero ICO.

- The key again is execution; the market doesn't believe the deal gets done, and definitely not at the $1bn+ valuation that’s been mooted for tZero.

Again, the mathematically astute reader will notice that *if* the GSR deal can be completed, Overstock’s holding in tZero will be worth more than the current valuation. This of course, places no value on the rest of Medici’s blockchain ventures. This, together with the potential from selling the retail business starts to create the convexity, and that’s without tZero or the blockchain businesses becoming something in the long-term.

Technical Accelerant

While OM believes the blockchain theme creates some long-term convexity, and the particulars of Overstock’s fundamental story creates short-term opportunity, it’s the technical factors that have the potential to act as accelerant to really drive the convexity.

A little backstory; Overstock came to Our Man’s attention after speaking with some short-sellers who having been short the name previously, were now long it. That is very rare! One, Marc Cohodes, was involved in litigation with Patrick Byrne (Overstock’s CEO) a decade+ ago. The pair recently settled their differences and Cohodes’ long position and strong views are well known.

While the presence of shorts-turned-longs is interesting, the accelerant is in the amount of short interest and the associated technical dynamics. At October-end, around ~1/3 of Overstock’s shares were short. This in a tightly held stock; Byrne and his family own around 1/3 of the stock, and that’s before you get to any other long-term holders. Accounting for this, 50%+ of the available float is currently short.

Should Overstock manage to execute well, then OM thinks the shorts scrambling to cover their positions will likely help create meaningful additional convexity. For the older financial folks amongst you, think a much scaled down version of Porsche/VW from 2008 as being the best case scenario.

Sizing

Our Man thinks that Overstock offers convexity in multiple ways, but he’s quite aware that (i) both the Blockchain theme and Overstock are potentially binary outcomes, and (ii) he could be 100% right on Blockchain and still lose all his $ in Overstock. As such, you should expect the Blockchain theme and the individual positions to be small, on a cost basis. Over the next couple of years, until either the stocks or the theme become less binary, OM will be biased towards taking profits rather than aggressively letting the position run. Overstock, and the Blockchain theme, are a ~2% position.

Disclaimer: OM is long Overstock (OSTK), as noted above.

- Overstock is in talks with GSR (a Chinese PE firm) who completed their legal due diligence in Q3. The deal involves taking a stake in tZero equity and a purchase of Overstock equity, in addition to GSR’s position in the recently completed tZero ICO.

- The key again is execution; the market doesn't believe the deal gets done, and definitely not at the $1bn+ valuation that’s been mooted for tZero.

Again, the mathematically astute reader will notice that *if* the GSR deal can be completed, Overstock’s holding in tZero will be worth more than the current valuation. This of course, places no value on the rest of Medici’s blockchain ventures. This, together with the potential from selling the retail business starts to create the convexity, and that’s without tZero or the blockchain businesses becoming something in the long-term.

Technical Accelerant

While OM believes the blockchain theme creates some long-term convexity, and the particulars of Overstock’s fundamental story creates short-term opportunity, it’s the technical factors that have the potential to act as accelerant to really drive the convexity.

A little backstory; Overstock came to Our Man’s attention after speaking with some short-sellers who having been short the name previously, were now long it. That is very rare! One, Marc Cohodes, was involved in litigation with Patrick Byrne (Overstock’s CEO) a decade+ ago. The pair recently settled their differences and Cohodes’ long position and strong views are well known.

While the presence of shorts-turned-longs is interesting, the accelerant is in the amount of short interest and the associated technical dynamics. At October-end, around ~1/3 of Overstock’s shares were short. This in a tightly held stock; Byrne and his family own around 1/3 of the stock, and that’s before you get to any other long-term holders. Accounting for this, 50%+ of the available float is currently short.

Should Overstock manage to execute well, then OM thinks the shorts scrambling to cover their positions will likely help create meaningful additional convexity. For the older financial folks amongst you, think a much scaled down version of Porsche/VW from 2008 as being the best case scenario.

Sizing

Our Man thinks that Overstock offers convexity in multiple ways, but he’s quite aware that (i) both the Blockchain theme and Overstock are potentially binary outcomes, and (ii) he could be 100% right on Blockchain and still lose all his $ in Overstock. As such, you should expect the Blockchain theme and the individual positions to be small, on a cost basis. Over the next couple of years, until either the stocks or the theme become less binary, OM will be biased towards taking profits rather than aggressively letting the position run. Overstock, and the Blockchain theme, are a ~2% position.

Disclaimer: OM is long Overstock (OSTK), as noted above.

Saturday, December 1

Things from my Newsblur; 2018 Part V

Time

for (probably) the final 2018 edition of “Things from my Newsblur”. As usual, the most investment-related stuff

is at the end, though this version does give a glimpse at a future theme and an

update on Greece. Before that it’s a

mixed bag of spying, left turns, Fortnite, London Underground and music!

This is the most important story written this year; it’s about a

unit of the Chinese PLA allegedly embedding tiny microchips in server

motherboards bound for US corporations. Either

Bloomberg have researched and written an exceptional exposé that suggests every

national security fear about “made in China” isn’t nearly paranoid enough. Or this is one of the most irresponsible and

dangerous pieces of journalism in many years; “fake news” would be a massive

understatement. Since the original

story, both Apple and Amazon have pushed back exceptionally aggressively on

this story with Tim

Cook (Apple CEO) demanding a retraction and Amazon’s Chief Security

Officer, Stephen Schmidt, providing an adamant

and clear rejection of the story.

Bloomberg for its part doubled

down, with a follow-up story a few days later.

(Jordan Robertson & Michael Riley, Bloomberg Businessweek)

A great article on how a small, cheap and simple change –

installing various rubber items at intersections where there are left turns –

is improving pedestrian safety in NYC.

The greater incidence of pedestrian injury when cars make left turns was

known for a while, but not understood.

NYC combed through its trove of data on accidents, finding that left

turns by cars cause 3x as many pedestrian and bicycle casualties as right-turns. Armed with the data, they studied the causes

and came up with a redesign of the streets that is both simple and cheap! Government can work sometimes!

(Karen Hao & Amanda Shendruk, Quartz)

Thankfully, OM’s kids aren’t old enough to play Fortnite because

if they were at least one (no prizes for guessing which one) would definitely

be addicted! This article looks at how

Fortnite has become a crazy phenomenon and some of the behavioral and

psychological tricks it’s employing to stay there.

(Nick Paumgarten, New Yorker)

Our Man’s first job saw him battle the masses at Bank station a

couple of times each day; it isn’t a cherished memory. This look at the challenging renovation of

the entire Bank/Monument train stations complex is fascinating. Amazingly, Transport for London opted for the

most innovative option and the result will be a truly transformational change,

despite substantial engineering and construction challenges. What challenges? Well it’s all taking place deep underground,

and there is one small rectangular shaft through which everything (including

the diggers) has to descend. The process

has been described as

trying to redecorate your living room with all the items being sent in through

your letterbox.

(Ian, at his blog Ian Visits).

An oral history on the back story of how the ubiquitous compilation

series came to rule the market.

Amazingly, it continues to prove resistant to the numerous

playlists/compilations available through online streaming. It sold an amazing 3.2million albums in the

UK in 2017, managing to outsell the leading artist (Ed Sheeran).

(Mark Savage, BBC)

Marc Andreessen’s seminal WSJ article that “Why

Software Is Eating the World” came out over 7-years ago, thus we cannot be

surprised by its increasing prevalence in our lives. This blog post by Tren Griffin highlights how

the emergence of mobile and the cloud has led to a new subscription based business

model for software companies that is both increasing their reach and speeding

up the pace of change. Subscription

business models in software (think Netflix, as the most basic example) will

have profound changes across the economy.

Why? It is an almost 0% marginal

cost business – that is, once the code is written it is infinitely divisible

(me watching Yes, Minister on Netflix doesn’t affect you watching it on

Netflix, at the same time!) and distribution costs via the cloud are negligible

(i.e. no producing disks, packaging, paying for retail space, etc.). This affects simple financial metrics (like

total addressable market and company valuation) but also has profound impacts on

more important things like employment. It

isn’t robots (like C3PO) that’s going to take your job but software that

automates parts of it and makes businesses more efficient. This will also start to disproportionately

impact white collar jobs that have been largely immune from the technological

changes of the last decade. Think of the

payroll software that means you need 3-4 people in that department not 5-6, or

the legal software that does large parts of a junior person’s case research.

(Tren Griffin, at his blog 25IQ)

[Spoiler Alert – Can you see a Software Thematic position coming

soon…]

Greece is the word, people!

You know OM has previously mentioned that he thinks Greece will be the

largest position in the portfolio at some point next year. Everything is slowly but surely lining up;

it’s exceptionally cheap, the fundamentals are improving yet are being ignored

because it’s hated. Our Man is hoping

2019 sees the technicals bottom and that the upcoming elections set the stage

for the narrative to change and investors to return. Thankfully, Lyall Taylor’s long but excellent

post saved Our Man having to write about the difference between the improving

reality and people’s assumptions! (Lyall

Taylor, at his blog The LT3000 Blog)

Subscribe to:

Comments (Atom)