Our Man followed through with the things on his docket last week, reducing the portfolio’s exposure about 8-10% above Thursday's market bottom. Frankly, OM hopes it’s a decision that looks abysmal in the future, since that likely means that COVID-19 came and passed quickly with limited impact.

The primary rationale for it was a combination of material year-to-date losses, increasing evidence of the West’s questionable handling of the COVID-19 outbreak, and the increased uncertainty caused by COVID-19.

- The losses began with Shipping’s sell-off in January and accelerated last week, as emerging market indices collapsed.

- It appears that most of the Western governments were caught off-guard by the spread of COVID-19, and reacting to events rather than having proactive plans. Bizarrely, the UK is an exception; it has a very clear plan though it is highly controversial and has been at least partially misunderstood. If you’re in the UK you must read Azeem Azhar’s newsletter post on it. If you're not in the UK, you should read it anyway.

- The uncertainty around COVID-19’s impact is worth discussing as ideally one should be a buyer in weeks like last week when there is “blood in the streets”. The argument for buying now is that this too shall pass, and numerous high quality stocks cheap on historical (or post-COVID-19) earnings. Thus buying today is right, even if there’s another 10-20% downside, as these names will be markedly higher in 12-months’ time. Normally, OM would nod in agreement. However, with COVID-19’s spread to Europe and the Americas, the weak response and the potential multiple week lock-downs ahead OM believes the range of outcomes is exceptionally wide. In the best case, it will look like nothing more than your typical economic or market slowdown and OM’s decision will be costly. However, the impacts of a prolonged lock-down are non-linear; too many (both large and small) businesses have too thin margins, too many fixed costs, and too much debt to be able to survive with limited revenue for that long. That starts to raise questions of the health of the economy we'll come back to post COVID-19. OM suspects that in many scenarios, the solution is going to look a lot like MMT.

Portfolio Changes

The planned reductions to the portfolio were discussed in the previous post but were:

- Technical Book: The Technical Book’s sell signal flashed in the final days of February, but OM waited for a meaningful bounce that never really came. He exited it at the close (thankfully!) on Friday, but the delay (vs. the first trading day of March) cost a couple hundred bps!

- Greece: OM cut this back materially. It was the only particularly hard decision in the reduction of exposure. The new government in Greece is largely doing very good job, including their fast response to COVID-19, but it doesn’t matter. The economic rebound is going to be tested by COVID-19’s impact on tourism among other things, and Greek equities are going to get limited attention from investors. The Greece ETF is trading below the levels when folks thought the country was run by a Crazy Leftist and about to leave the euro for the drachma. This is why it’s still the 2nd largest position in the book.

- Brazil, India & Vietnam: Both Brazil and India saw their first COVID-19 cases during the week, which led to OM to slightly increase his reduction in those positions. Longer-term, Vietnam continues to a beneficiary of broadening supply chains but was also reduced.

- SaaS & Uranium: The exposure to the older ETFs was cut back. There are some more recently launched ETFs that better fit the theses, and OM will be adding these when the moment comes. OM also trimmed back the JD.com position, which is up for the year.

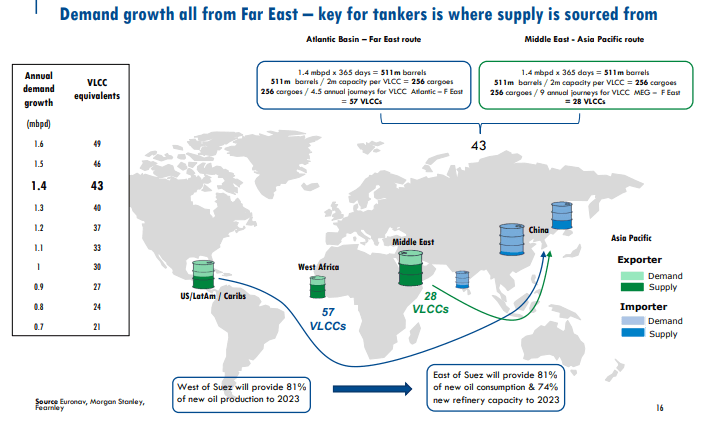

OM also bought some more crude and oil product tankers!

In the week since OM’s last post on Shipping, Saudi Arabia and Russia started an all-out price water which saw oil prices tumble 30%+. The combination of the attractiveness of storing crude & oil products and the Saudis hitting the bid on every VLCC tanker they could find saw tanker rates rise 4-8x last week! This is the start of the low season, but instead rates are printing at all-time highs; there are ships that are literally making a year’s worth of income in a single 45-day voyage!! OM added some Double Hull Tankers (DHT, crude tanker company with a fleet of VLCCs) but didn’t get filled in his attempt to buy Teekay Tankers (TNK). If these rates continue and the stocks don't reflect it, expect OM to continue to keep buying more of his existing positions (and TNK) till he hits 25% NAV. Given the cash flow that these companies are going to throw off in Q1 and Q2, OM is happy keeping this position at a much higher size though he’ll be selling lots of the rest of the portfolio to keep overall risk in check. OM exited the existing position in Navigator Holdings (NVGS), which is focused on liquid natural gas not crude and oil products.

Portfolio (as at 03/13/20 - all delta and leverage adjusted, as appropriate)

Dislocations: 31.0%

17.9% - Shipping (STNG, DSSI, EURN, DHT and NVGS)

9.9% - Greece (GREK, ALBKY, and EGFEY)

3.2% - Uranium (CCJ and NXE)

Thematic: 15.1%

5.2% - Tech 4th Industrial Revolution (JD & WCLD)

3.4% - Vietnam (VNM)

3.3% - Brazil (EWZ)

3.2% - India (INDA)

0.0% - Blockchain/Crypto (no positions)

Technical: 0.0%

0.0% - OEW Technical positions (DDM, SSO, and QLD)

Idiosyncratic: 16.9%

14.2% - Funds (ARTTX, CWS, GVAL, and CAPE)

2.6% - Equities (TPL)

Shorts/Hedges: 0.0%

Cash: 37.1%

Disclaimer: Nothing above represents a recommendation in any way, shape or form so please don’t even think of trying to take it that way. For added clarity, while Our Man is invested in all of the securities mentioned that’s a terrible reason for anyone else to do so. Our Man also holds some cash and a few other securities (of negligible value). You should not buy any of these securities because Our Man has mentioned them, but should do your own work and decide what’s best for you given your own circumstances/risk tolerance/etc.

{kind=link}