- European debt problems (and recession?)

While Draghi’s efforts have

enabled Europe’s weaker countries to have continued access to the debt markets,

they haven’t prevented a number of European companies from having tepid growth

or falling back into recession. The risk

in Europe continues to be further political breakdown driven by the weak growth

(or negative growth), especially if it persists in the stronger European

core. During 2013, some things to watch

will be the elections in a number of countries (especially whether we see an

anti-reform government in Italy, and what happens in Germany) and whether there

will further unrest in the austerity countries (especially Spain and Greece).

- China (and the rest of the BRICs)

While

China appears not to be a concern in the short-term, after growth picked up in

Q4, there continue to remain question marks over the veracity of the data. The other major concern over China’s growth

is the aggressive government-sponsored/encouraged expansion of credit, and whether

the sharp increases will feed through to higher NPLs.

- Japan

As

Our Man remarked last year, Japan is fascinating as they were the first country

into a debt-deflationary spiral and there’s a reasonable chance that they may

be the first country out of it. Both of the key pillars of Japan’s

strength, its savings rate and trade surplus, continue to wane and the new

government appears very inclined to pressure the BoJ into further QE by setting

a specific inflation target.

-

US Political Intransigence (or Incompetence)

Over

the last few years, one sad truth has been that we shouldn’t underestimate the

incompetence of politicians in Washington.

While 2013 seems to have started on a positive trend, with a fiscal

cliff deal and an agree to increase the debt ceiling in the short-term, there’s

ample opportunity for the sequester and budget hijinks to result in no deal and

a government shut-down, or one that has imposes much austerity too quickly and

only succeeds in pushing the economy back into recession.

- Negative Contagion

One of the great positives of 2012 was that we arguably

saw positive contagion, where positive developments spilled over from one area

to the next. The risk in 2013 is of

negative contagion, where negative events in one region impact the others; such

as a slowing Europe exacerbate the problems in China and Japan, which combined

with a budget stand-off helps pull the US towards recession.

- Global Trade & Protectionism

A

holdover from previous years! For those

who are historically minded, the steady decline of Global Trade and the rise of

protectionism was one of the noticeable features of the 1930's depression in the

US. With so many countries facing growth headwinds, and attempting to

encourage exports, the temptation for domestic politicians will continue to be

to blame foreigners and the rhetoric about punishing “cheating” (i.e. trade

surplus) countries will remain. Let’s hope we don’t see an equivalent of

the Kindleberger spiral for 2010’s!

-

Demographics

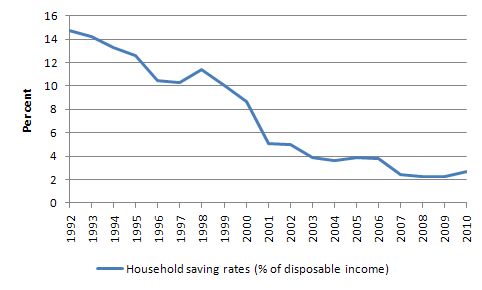

A

long-term concern for Our Man is the weak demographics of the Western

world. While this is a major problem in

Japan, China and many European countries, it’s also starting to impact the

US. In 2011, the US Birth Rate hit a

historic low (it’s now about ½ the peak rate of the baby boom years) and the US

fertility rate (1.9 children/woman) is now below the rate needed to maintain the

current population. Furthermore, the

aging of the baby boomers will continue to have significant impacts on housing,

employment and unemployment and investing.

- Corporate Margins & Valuation

Another

holdover from previous years! While all

the other ‘fingers of instability’ suggest risks to the global economies, it’s corporate margins and valuations

that make the market particularly vulnerable. While short-term

measures (such as trailing P/E or the awful forward Operating P/E) suggest that

the market is cheap/fairly valued they require the belief that the current

level of margins (near all-time highs) is sustainable ad infinitum.

Perhaps they are, and we’re in a new paradigm but Our Man suspects that

reality is that the elevated levels of margins offers more potential for

downside surprise than upside opportunity. While long-term measures of

valuation are a terrible guide to any given year’s market performance, they do

offer a valuable guide or map for real cheapness or value and they don’t

suggest that the broad equity markets offer much in the way of absolute value.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}